本次英国代写是一个投资组合管理的限时测试

MCQ1:

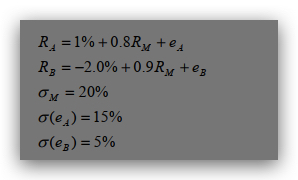

Assume that the index model for the excess returns of stocks A and B is estimated with

the following results:

The covariance of stock A and B is closest to

(a) 100

(b) 200

(c) 300

(d) 400

(e) 500

MCQ2:

The feature of the Arbitrage Pricing Theory (APT) that offers the greatest potential

advantage over the simple CAPM is the

(a) Identification of anticipated changes in production, inflation, and term structure of

interest rates as key factors explaining the risk-return relationship

(b) Superior measurement of the risk-free rate of return over historical time periods

(c) Variability of coefficients of sensitivity to the APT factors for a given asset over

time.

(d) Use of several factors instead of a single market index to explain the risk-return

relationship.

(e) Superior measurement of the market beta to reduce estimation error.

MCQ3:

Assume that both portfolios X and Y are well diversified, that E(rA)=12%, and E(rB)=9%.

If the economy has only one factor, and βA=1.2, whereas βB=0.8, what must be the risk

free rate? The risk-free rate is closest to

a) 1%

b) 3%

c) 4%

d) 5%

e) 6 %

MCQ4:

Roll’s critique describes the use of an incorrect benchmark (market proxy) portfolio as

a) Benchmark risk

b) Tracking error

c) Benchmark error

d) Measurement error

e) Market risk

MCQ5:

The Macaulay duration of a par-value bond with a coupon rate of 8% (paid

annually) and a remaining time to maturity of 5 years is

A. 5 years.

B. 5.4 years.

C. 4.17 years.

D. 4.31 years.

E. 3.82 years.