这是一个美国的高级企业考试金融代写

Question 1

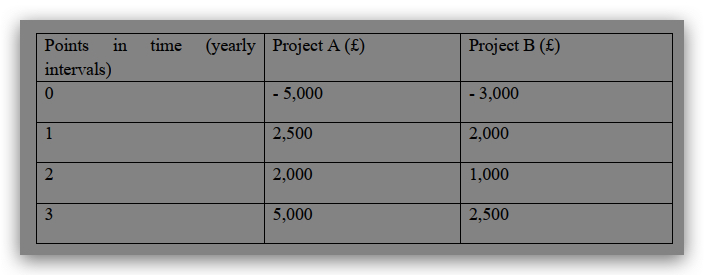

Two projects A and B have the following cash flows:

1) The Board of Directors has set 2 years as decision benchmark. Find the Payback periods

for the two projects. Which project would be accepted?

2) The discount rate is 10%. How would the NPV rule rank these two projects? And which

project would be accepted based on NPV if they are mutually exclusive?

3) Assuming now that the two projects are independent, would you accept them if the cost of

capital is now 15%?

4) The Board of Directors is considering installing an updated computer system in the business.

The investment outlay on the update will cost £45,000, 70% of which is payable immediately

with the remaining 30% payable in a year’s time. Installing this computer system update will

reduce the firm’s costs for six years with £11,500 annually for the first two years followed by

£8,000 annually in the next four years. Based on your calculation, advise The Board of

Directors whether the updated computer system is worth installing if its required rate of return

is 9%.

Question 2

The Treasury bill rate is 4%, and the expected return on the market portfolio is 12%. Using the Capital

Asset Pricing Model (CAPM):

1) Discuss how the expected return varies with the beta. Calculate the market risk premium and the

required return on an investment with a beta of 1.20.

2) If an investment with a beta of 0.7 offers an expected return of 9%, does it have a positive NPV?

3) If the market expects a return of 15% from stock A, what is its beta?

4) Critically evaluate the main assumptions upon which the CAPM model is based.

Question 3

(a) Discuss the difference between forward and futures contract.

(b) On the 20th November 2021, the spot price of wheat is $3.00/bushel. The net convenience yield is

5% per month. If the risk-free rate is 4% per year, calculate the six-months future price.

(c) Explain how a wheat producer would use a futures market to lock in the selling price of a planned

shipment of 1,000 bushels of wheat six months from now

(d) Suppose the producer takes the actions recommended in your answer to (c), but after one month

wheat prices have fallen to $2.00/bushel. What happens? Will the producer have to undertake

additional futures market trades to restore its hedged position?

(e) If the net convenience yield for the wheat now is18% per year. The risk-free interest rate is still

4% per year. What is the six-months future price for wheat?

Question 4

(a) Assume that you buy a call with an exercise price of $100 and a cost of $9. At the same

time, you sell a call with an exercise price of $110 and a cost of $5. The two calls have

the same underlying stock and the same expiration.

(i) Graph the profits and losses at expiration from this position