本次美国作业是Matlab金融数据分析的一个assignment金融代写

Instructions: Type out your work in a readable form using a document editor of your choice.

Also attach the Matlab code of your work to the submission on Canvas. Code should be easy-to-read and should be able to run from my work station without any difficulty. Do not include any irrelevant code or texts. Set rng(‘default’) for Matlab simulation so that I may check your work.

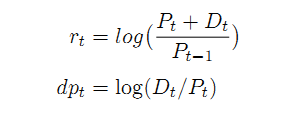

1. The dataset data1945 2015.xlsx gives the real price Pt and dividend series of US stock

market index Dt over years 1945∼2015. Using this dataset and Matlab with your own code,

compute and save two variables, continuously compounded returns(including dividends) rt,

and log dividend-price ratio dpt for the exercises below.

a. Using the log dividend-price ratio as the predictor forecasting the return one-step-ahead,

run a predictive regression of form rt = α+dpt−1β +ϵt using least squares. Report the

R-square, the slope estimate, t-statistic for the two-sided test of predictability, and its

p-value.

b. Calculate (1) the Stambaugh estimator for β and (2)the Jackknife estimator of β

based on (approximately) equally dividing the whole sample into three subsamples.

Compare your results.

c. Run the horizon-8 predictive regression of rt on dpt−1: Report the direct estimator(OLS)

of the horizon-8 regression slope and R-square.

d. Using AR(1) model via dividend-price-ratios as xt, report the implied estimator for the

horizon-8 regression slope and R-square. You may use any built-in resources you can

find in Matlab to do this.